Costa Coffee, Starbucks and Caffè Nero remain the UK’s largest coffee shop chains by outlet numbers

- The £10.1bn UK coffee shop market grew by 7.9% in turnover during 2018, representing 20 consecutive years of sales and outlet growth

- Most industry leaders say Brexit uncertainty is negatively impacting trade and consumer confidence, which could blow sector off course in 2019

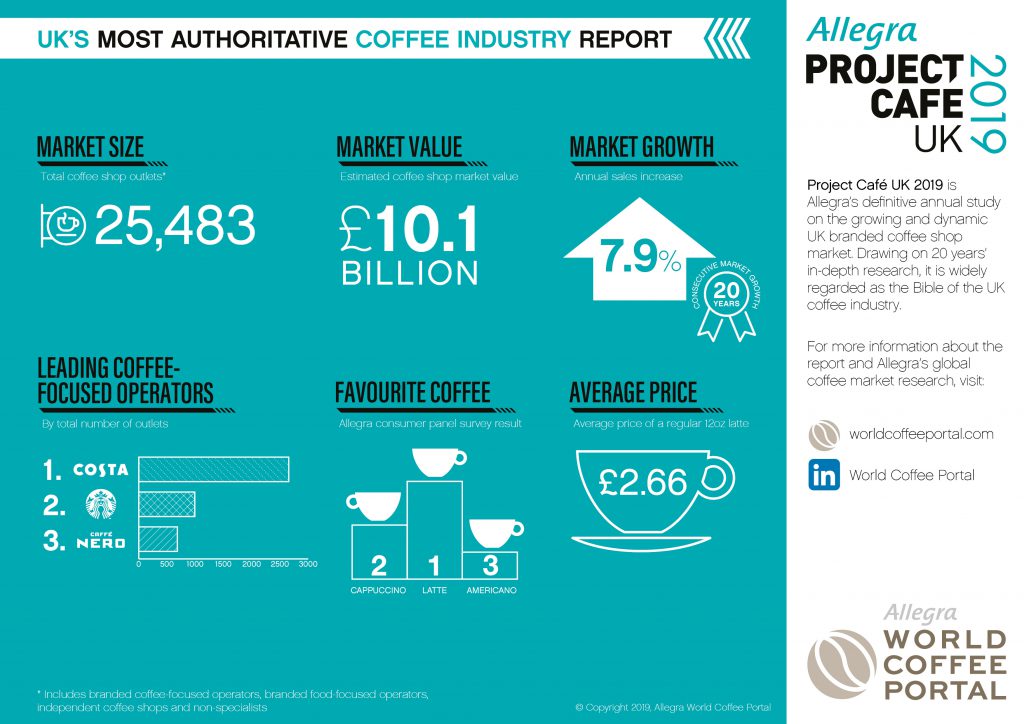

Project Café UK 2019, Allegra World Coffee Portal’s market-leading report on the UK café industry, reveals the total UK coffee shop market is valued at £10.1bn across 25,483 outlets*. A 7.9% annual sales increase cemented two decades of UK coffee shop growth, but economic turbulence caused by Brexit uncertainty continues to impede the sector.

Resilient coffee shops outperform troubled UK high street

Branded coffee shops secured robust 8.7% outlet growth in 2018 to reach 8,149 stores. The fragility of the UK economy is, however, a key industry concern for 2019. Coffee shops are a vital piece of the UK high street fabric, with widespread retail closures exacerbating reduced footfall for all businesses.

Allegra research shows coffee shops are well placed to catalyse growing consumer preference for experience-led and digitally-enhanced retail concepts – 45% of industry leaders surveyed consider social media to be the most effective form of marketing. However, coffee quality remains the biggest factor behind café success according to industry leaders surveyed by Allegra.

Reduced consumer confidence contributed to the success of value-focused chains in 2018. Allegra consumer data shows Greggs and McDonald’s are perceived to offer the best value-for-money, with both brands introducing coffee-focused strategies in 2018.

Most industry leaders indicate Brexit is negatively impacting trade

Sustained uncertainty on the UK’s future relationship with the EU continued to frustrate the coffee shop industry in 2018. The political impasse over the last 18 months has contributed to growing anxiety on labour shortages, rising prices, investment and eroded consumer confidence.

49% of industry leaders surveyed by Allegra indicated Brexit was negatively affecting their business, with 46% remaining neutral and 5% reporting a positive impact. 69% agreed it was negatively impacting consumer confidence, while 87% of industry leaders surveyed believe Brexit has damaged the UK economy.

Consolidation and premiumisation reshape the UK coffee shop landscape

The UK coffee shop market experienced significant consolidation in the last 18 months. Major deals such as Coca-Cola’s £3.9bn acquisition of UK market leader, Costa Coffee, and JAB Holding’s £1.5bn acquisition of Pret A Manger have introduced unprecedented foreign investment into the UK branded coffee chain market.

In the specialty segment, a burgeoning 5th Wave of scaled artisan concepts continues to grow and promote market-wide premiumisation. Department of Coffee and Social Affairs acquired several independent café businesses to increase its portfolio to 22 stores in 2018. London-based Grind continues to develop its travel hub partnership with SSP, and Caravan has expanded its portfolio with private investment firm, Active Partners.

Coffee-focused segment achieves 8.1% outlet growth

Costa Coffee, Starbucks and Caffè Nero remain the three largest coffee-focused branded chains in the UK, with 2,655 outlets, 992 and 683 stores respectively.

Allegra forecasts the UK branded coffee shop market will exceed 10,000 outlets by 2023, displaying 5-year compound annual growth rate of 5%.

Commenting on the research, Allegra CEO, Jeffrey Young said: “20 years of consecutive growth, in terms of outlets, turnover and like-for-like performance is an impressive feat by this robust segment that has become intrinsic to UK lifestyles. More growth will continue, albeit at a slower pace, as the economy is subjected to myriad pressures, including structural retail change, technological development, changing consumer habits and deep uncertainty on the numerous potential outcomes of Brexit.”

***

*Includes branded coffee-focused operators, branded food-focused operators, independent coffee shops and non-specialists

Analysis by Allegra World Coffee Portal

Words: Tobias Pearce

There are 0 comments